Microsoft (MSFT): AI Leadership Supports Long-Term Growth

$396.94

21 Jul 2026, 22:43

Neutral

Join Minipip Academy and access free courses in investing, trading, economics, and more.

Sign Up

S&P 500 Analysis: Growth Strength Meets Macro Constraints

The S&P 500 serves as a benchmark for the performance of the US equity market, representing approximately 80% of total market capitalisation. Unlike individual stocks, where fundamental analysis focuses on company-specific financials, analysing an index requires a broader, top-down approach that examines the macroeconomic environment, including fiscal and monetary policy.

Macroeconomic Environment

The US economy remains relatively strong, with GDP growth continuing to exceed expectations in recent quarters, supported by robust consumer spending and ongoing investment. Strong economic output typically acts as a bullish driver for equities, as it supports higher revenues and earnings. However, it simultaneously reduces the need for monetary easing from the Federal Reserve, keeping interest rates elevated. This sustains tighter financial conditions, limiting valuation expansion and capping equity upside despite positive growth dynamics.

Monetary Policy & Interest Rates

Monetary policy remains a dominant driver of index performance. The Federal Reserve has maintained the federal funds target range at 3.50%–3.75%, following a series of rate cuts in late 2025. While this represents a shift away from peak restrictive levels, policy remains tight.

Interest rates influence the S&P 500 through several key mechanisms:

Inflation

With projections indicating levels above 3% through the first half of 2026, persistent price pressures, particularly in energy and goods, continue to impact both consumers and corporate margins.

In the short term, rising inflation tends to weigh on equities by:

The S&P 500 has demonstrated resilience despite elevated inflation, largely due to strong earnings growth and investor confidence in long-term structural trends such as AI.

Earnings & Valuation

Corporate earnings remain the primary fundamental support for the index. Strong GDP growth and continued investment have driven robust earnings expansion across the S&P 500.

While price-to-earnings ratios remain elevated relative to historical averages, forward earnings expectations have continued to rise, helping justify current price levels.

This dynamic suggests that:

Labour Market Conditions

Equity markets are inherently forward-looking, responding less to current economic conditions and more to expectations of future policy and liquidity. The interaction between the labour market and monetary policy is therefore a key driver of market sentiment.

As of April 2026, the U.S. labour market is showing early signs of cooling, with unemployment easing slightly to 4.3% in March after peaking at 4.5% in late 2025. At the same time, the Federal Reserve has maintained a cautious stance in balancing persistent inflation against signs of slowing job growth.

In this context, moderate increases in unemployment can be interpreted positively by equity markets when they signal a likelihood of future monetary easing. As a result, weakening labour data, under certain conditions, may act as a catalyst for equities.

Geopolitical & External Risks

Geopolitical developments are influencing the S&P500 primarily through energy markets, where tensions involving Iran and potential disruptions in the Strait of Hormuz have pushed oil prices above $100 per barrel, reinforcing inflationary pressures and delaying expected rate cuts from the Federal Reserve. This creates a ‘higher-for-longer’ rate environment that limits valuation expansion, even as earnings remain resilient, with projections of 12–19% growth in 2026. Despite elevated oil prices, the index has shown relative strength, partly due to the U.S. acting as a net energy exporter, but this masks growing sector divergence, with energy stocks outperforming sharply while transportation, industrials, and consumer discretionary sectors face margin pressure.

As a result, markets are currently balancing strong earnings and AI-driven growth against rising macro risks, with sentiment driven by short-term geopolitical developments such as ceasefire expectations, while the risk of a sustained oil shock, particularly above the $130 mark, remains a key downside trigger for both economic growth and equity performance.

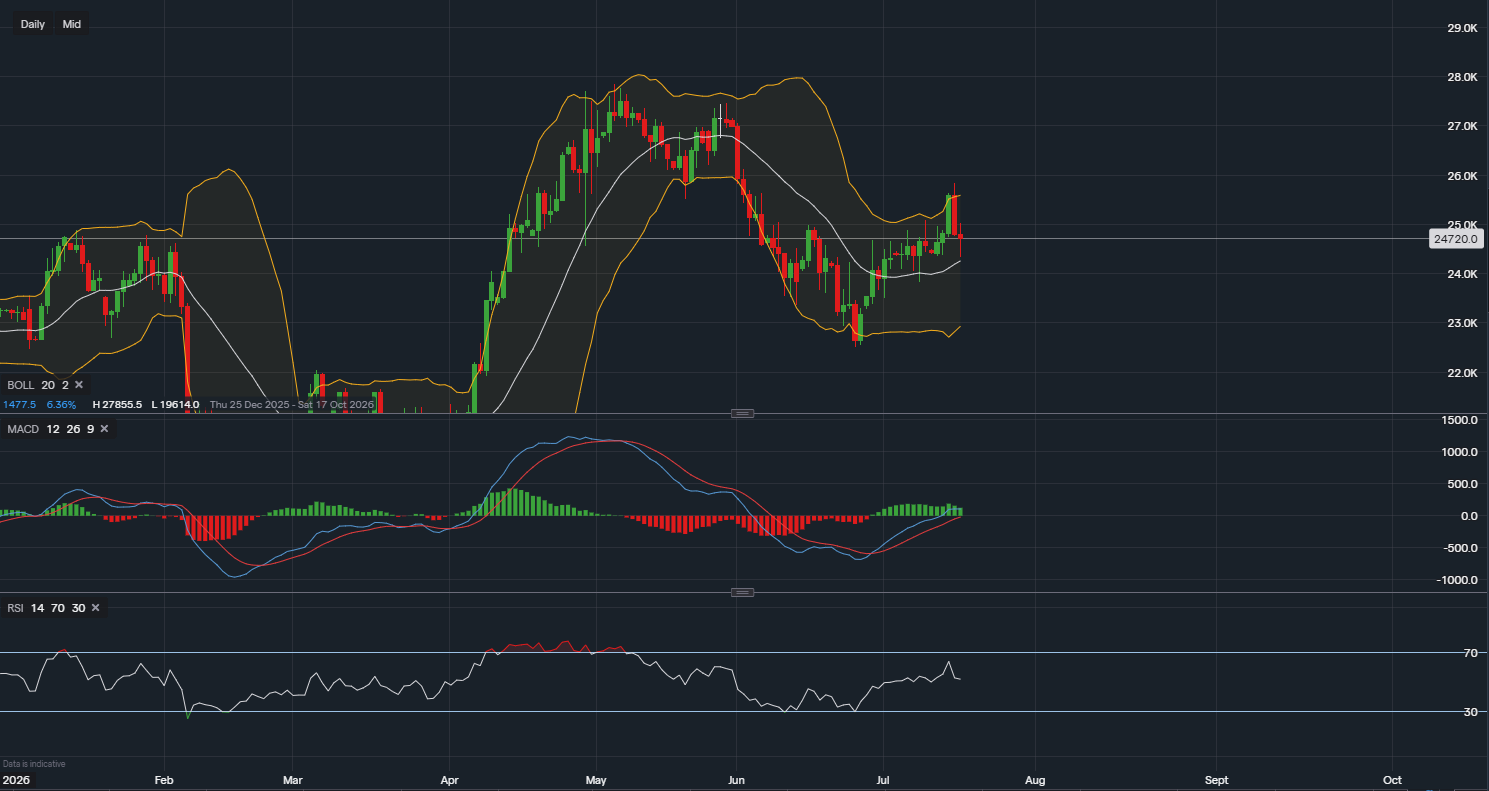

Price Action & Technical Analysis

The S&P 500 is currently trading at 6955.79, maintaining a confirmed bullish trend following a strong rebound from the 6300 support zone. This recovery has established a clear upward price structure, with the index now approaching a key resistance area formed during the January–February period, marking an important test for further continuation.

Price is trading well above the Ichimoku cloud, with the conversion line (6718) positioned above the base line (6643), and the lagging span also confirming bullish alignment. This reflects a strong trend regime with both momentum and structure favouring the upside. Similarly, the moving average structure reinforces this outlook. While the 20-period EMA (6711) remains slightly below the 50-period EMA (6736), indicating a short-term lag, price is positioned above all major averages, and the 50 EMA remains above the 200 EMA (6615), confirming a sustained bullish trend on a broader timeframe. This suggests that short-term price action is catching up with an already established medium- to long-term upward trend.

Momentum and trend strength indicators further support this bullish outlook. The Directional Movement Index shows +DI (24.22) exceeding –DI (21.41), indicating that buyers retain control, while an ADX reading of 32.39 confirms that the current trend is strong and strengthening. Volatility conditions are also expanding, with Bollinger Bands widening as price pushes along the upper band. This is supported by the MACD, which shows a strong bullish crossover with a significantly positive histogram, reflecting accelerating upward momentum.

The Relative Strength Index (RSI) currently sits at 67.64, placing it within the upper momentum range but not yet in extreme overbought territory. In the context of a strong trend, this may suggest sustained buying pressure with the potential for RSI to remain elevated.

Overall, the technical picture remains bullish, with strong trend alignment, increasing momentum, and expanding volatility supporting further upside potential. However, with price approaching a key resistance zone, the index is at a critical point. A confirmed breakout above this level would reinforce continuation of the current trend, while rejection could lead to a period of consolidation or a short-term pullback before any further directional move.

Conclusion

Overall, the fundamental backdrop for the S&P 500 can be described as supportive but constrained. Strong economic growth and earnings expansion continue to underpin the market, while persistent inflation, elevated interest rates, and geopolitical risks limit the scope for sustained upside.

From a technical perspective, the index remains in a confirmed bullish trend, supported by strong momentum and trend alignment across multiple indicators.

Taken together, the S&P 500 appears positioned for continued upside bias, but within a more volatile and conditional environment. Further gains are likely to depend on the market’s ability to sustain earnings growth and break through resistance, while downside risks remain tied to inflation persistence, shifts in Federal Reserve policy, and escalation in global geopolitical tensions.

Educational Disclaimer

This content is for educational and informational purposes only and should not be considered financial advice. Always conduct independent research or consult a qualified financial professional before making investment decisions.

Tradable assets:

Min.Deposit:

Max Leverage:

FCA:

Rating:

Earnings Calendar

Earnings Calendar  Economic Calendar

Economic Calendar  VAT Calculator

VAT Calculator  Tax Free Childcare Calculator

Tax Free Childcare Calculator Percentage Calculator

Percentage Calculator Compound Interest Calculator

Compound Interest Calculator  Loan Overpayment Calculator

Loan Overpayment Calculator Mortgage Calculator

Mortgage Calculator Credit Card Calculator

Credit Card Calculator

Investing

Investing  Economics

Economics Trading

Trading  Technical Analysis

Technical Analysis  Personal Finance

Personal Finance Calculator

Calculator