Visa Stock Analysis: Bullish Momentum Builds Ahead of Earnings

$355.74

27 Jul 2026, 14:37

Bullish

Join Minipip Academy and access free courses in investing, trading, economics, and more.

Sign Up

UnitedHealth Group Analysis: Defensive Healthcare Scale Amid Regulatory and Margin Pressures

UnitedHealth Group is one of the largest healthcare institutions in the United States, benefiting from substantial institutional ownership, high market liquidity, and diversified operations across insurance and medical services.

Its scale within the Healthcare Plans industry provides relatively stable and inelastic demand compared to more cyclical sectors, making the company an important defensive component within a portfolio capital rotates towards healthcare during uncertain macroeconomic conditions.

Fundamental Snapshot

UnitedHealth Group currently trades at a trailing P/E ratio of 30.64, up from 29.62 last month, compared to a forward P/E of 19.4, which itself has risen from 18.88. The moderate compression suggests that markets are pricing in expectations of future earnings recovery and operational stabilisation. The projected earnings estimate of $19 billion has fallen from a previous estimate of $20.83 billion indicates the market is expecting higher costs to dent future cash-flow however, comparing this to current trailing earnings of $12.04 billion, reinforces the forward-growth narrative. Meanwhile, the PEG ratio of 1.3 suggests valuation remains relatively balanced against expected growth. A market capitalisation of approximately $368.39 billion, rising from $356 billion, further reflects the company’s systemic importance within both the healthcare sector and broader portfolio allocation in institutional finance.

From a balance-sheet perspective, the debt-to-equity ratio of 0.80 indicates moderate leverage that remains manageable for a company with strong recurring cash-flow generation and defensive healthcare exposure. The price-to-book ratio of 3.76 implies investors continue assigning a premium valuation to the company’s scale, profitability, and long-term earnings durability rather than valuing the business purely on tangible assets alone. Collectively, these metrics suggest that investors currently view UnitedHealth as a mature but still expanding healthcare institution capable of sustaining operational growth, although future valuation expansion remains highly dependent upon the company’s ability to control medical-cost inflation, preserve margins, and navigate increasing regulatory and reimbursement pressures.

Analyst Consensus & Market Expectations

Analyst sentiment toward UnitedHealth Group remains moderately bullish, with 19 buy ratings, 3 hold ratings, and only 1 sell recommendation across 23 analyst assessments, although the average price target of $406.09 implies very slight near-term up- and downside, a figure currently oscillating between -1% and 1%. The bullish thesis is largely driven by the company’s strong free-cash-flow generation, diversified healthcare ecosystem across UnitedHealthcare and Optum, and ongoing AI-driven operational efficiencies aimed at reducing administrative costs and improving long-term productivity. However, analysts also remain cautious regarding membership-growth pressures within Medicare and ACA segments, rising medical-cost inflation, margin compression, declining return-on-equity trends, and increasing regulatory risks surrounding reimbursement models, Medicaid funding, and pharmacy-related legislation, all of which can materially affect future profitability and increase the risk for earnings durability.

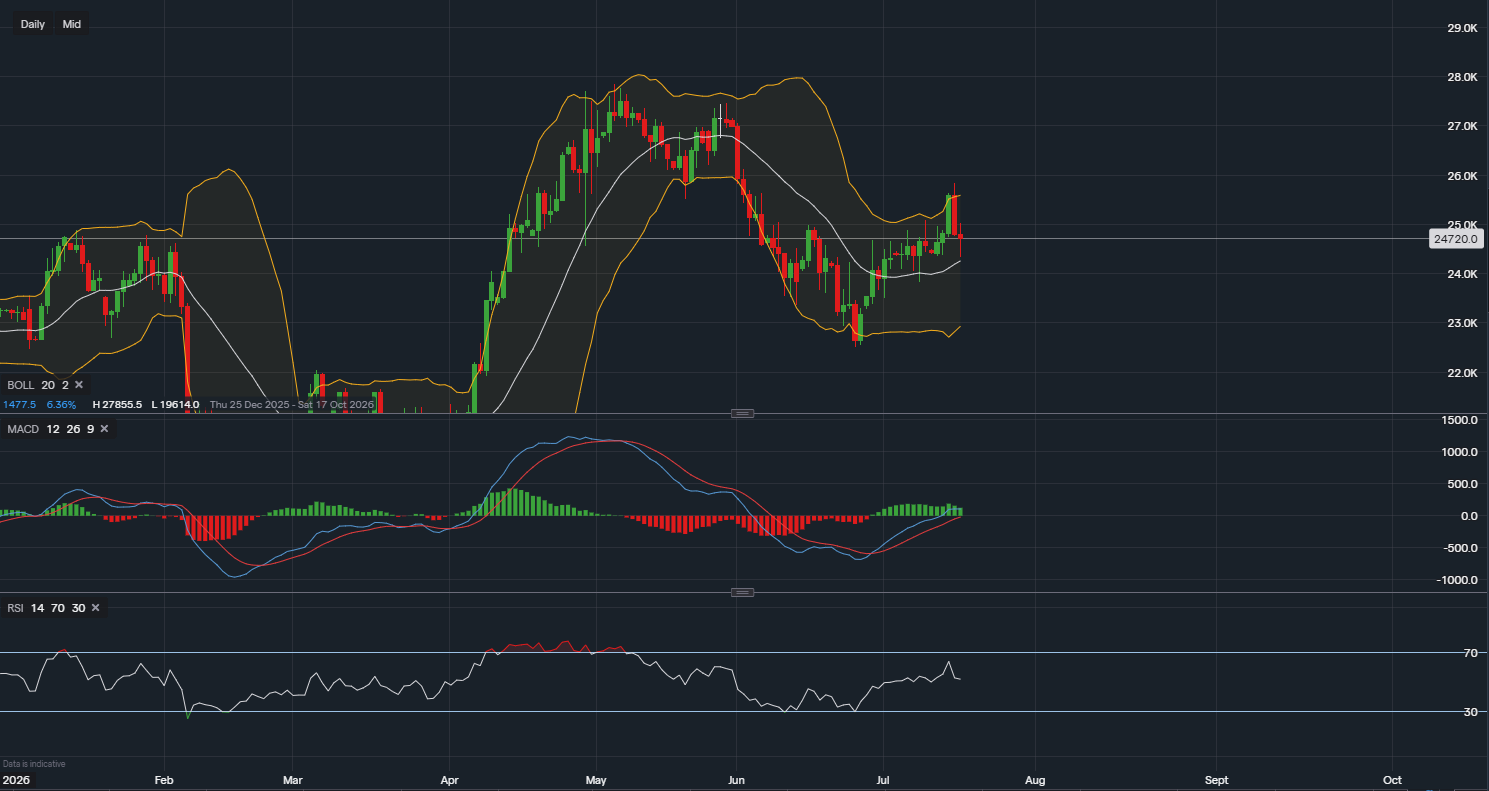

Price Action & Technical Analysis

UnitedHealth Group currently remains within a strong bullish recovery structure across multiple timeframes. The EMA alignment is technically constructive, with price trading above the 20 EMA (392), 50 EMA (370), and 100 EMA (349), while the moving averages themselves remain positively stacked. This configuration typically reflects sustained bullish trend continuation and institutional capital flow. The Directional Movement Index further reinforces this interpretation, with +DI (33) materially above –DI (10), while the ADX reading of 43 suggests an exceptionally strong established trend.

Momentum indicators, however, suggest the trend may be entering a more mature stage. The RSI reading of 66 approaches overbought territory, indicating elevated bullish momentum but also increasing susceptibility to short-term consolidation or pullback behaviour. Similarly, although price continues trading near the upper Bollinger Band (414), the MACD line slightly above the signal line suggests bullish momentum may start to increase slightly after a period of deceleration. From a price-action perspective, the short-term trend remains bullish, the medium-term trend remains strongly bullish, and the long-term structure continues to reflect a broader recovery trend following prior downside pressure.

Immediate support is located near the 20 EMA region. Resistance is currently concentrated between 404 which is currently being tested.

Conclusion

While institutional sentiment remains moderately bullish, rising medical-cost inflation, regulatory pressure, and margin compression continue to present medium-term risks, suggesting the stock currently reflects a balance between long-term operational resilience and increasing structural healthcare-sector uncertainty.

Educational Disclaimer

This content is for educational and informational purposes only and should not be considered financial advice. Always conduct independent research or consult a qualified financial professional before making investment decisions.

Tradable assets:

Min.Deposit:

Max Leverage:

FCA:

Rating:

Earnings Calendar

Earnings Calendar  Economic Calendar

Economic Calendar  VAT Calculator

VAT Calculator  Tax Free Childcare Calculator

Tax Free Childcare Calculator Percentage Calculator

Percentage Calculator Compound Interest Calculator

Compound Interest Calculator  Loan Overpayment Calculator

Loan Overpayment Calculator Mortgage Calculator

Mortgage Calculator Credit Card Calculator

Credit Card Calculator

Investing

Investing  Economics

Economics Trading

Trading  Technical Analysis

Technical Analysis  Personal Finance

Personal Finance Calculator

Calculator