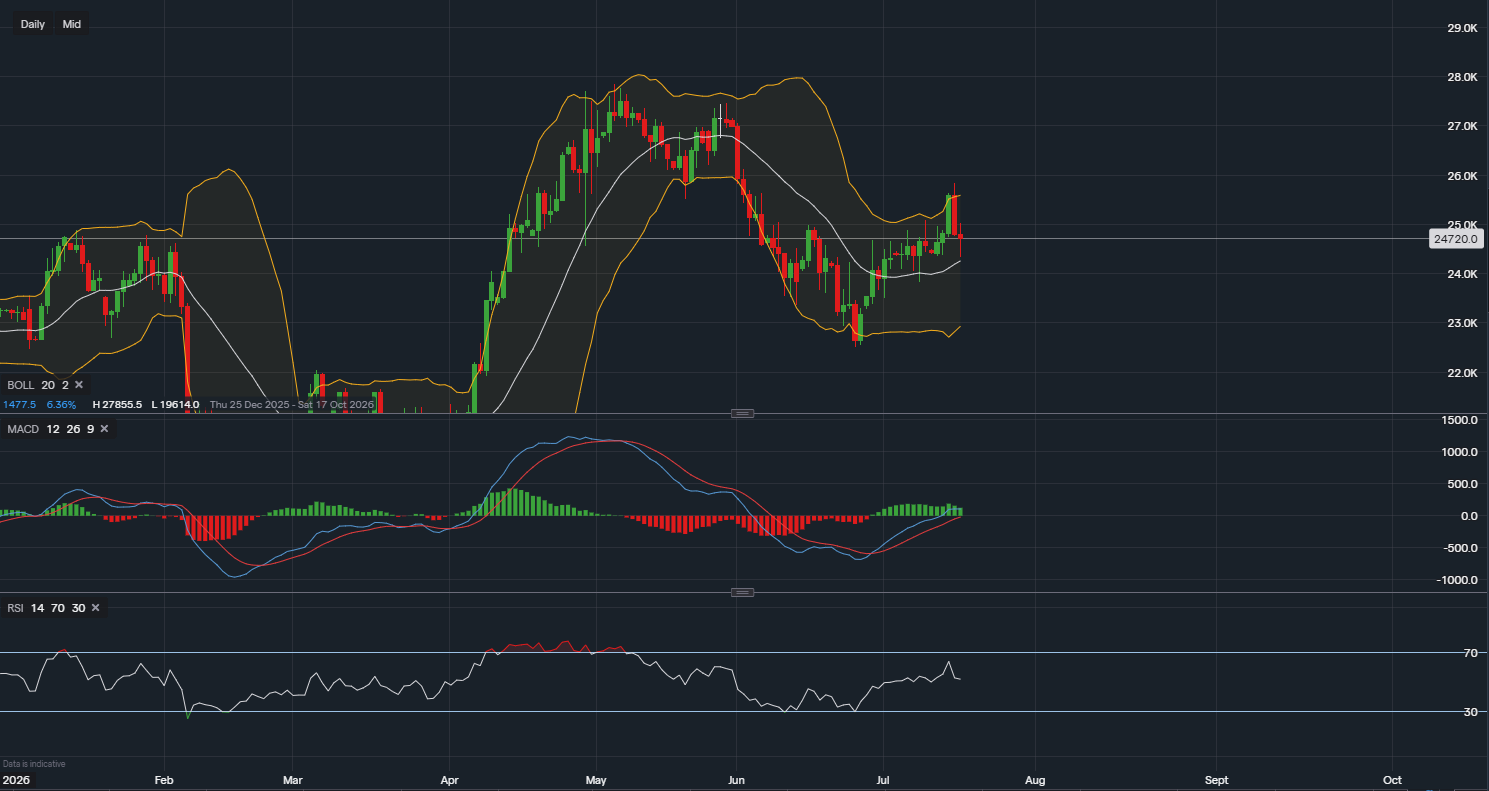

Visa Stock Analysis: Bullish Momentum Builds Ahead of Earnings

$355.74

27 Jul 2026, 14:37

Bullish

Join Minipip Academy and access free courses in investing, trading, economics, and more.

Sign Up

Pexels.com

Simple UK gifting rules that could help protect your family from an unexpected HMRC bill.

Gifting money to children, grandchildren or other loved ones can be a sensible way to support them during your lifetime. However, in the UK, gifts are not always completely tax-free. Depending on the size of the gift and when it was made, HMRC may still treat it as part of your estate for inheritance tax purposes.

Inheritance tax is usually charged at 40% on the value of an estate above the available tax-free threshold. The standard nil-rate band is currently £325,000, while an additional residence nil-rate band may apply when a qualifying home is left to direct descendants.

The key rule to understand is the seven-year rule. If you give away money, property or valuable possessions and survive for seven years, the gift is usually outside your estate for inheritance tax purposes. If you die within seven years, the gift may still be counted.

How much can you gift tax-free?

There are several inheritance tax exemptions that can help people pass on wealth more efficiently.

The main tax-free gifting allowances include:

The useful but overlooked income gifting rule

One of the most valuable exemptions is known as normal expenditure out of income. This allows regular gifts to be made from surplus income, rather than savings or capital.

To qualify, the gifts must:

Examples may include helping a child with rent, paying into a child’s savings account or supporting an elderly relative.

How does HMRC find out about gifts?

Most straightforward cash gifts do not need to be reported to HMRC when they are made. Instead, gifts are usually reviewed after death when executors deal with the estate.

Executors may need to check:

If gifts are missed and inheritance tax is underpaid, HMRC may charge penalties or seek payment from the estate.

Conclusion

Gifting money can be a useful way to support loved ones and reduce a future inheritance tax bill, but it must be planned carefully. The safest approach is to understand the allowances, keep clear records and avoid leaving family members with confusion after death.

For larger gifts, regular income gifts or estate planning, it may be worth speaking to a qualified tax adviser or financial planner. Used correctly, gifting can be a powerful part of long-term inheritance tax planning.

Sources: (SKYMoney.com, Gov.UK)

Tradable assets:

Min.Deposit:

Max Leverage:

FCA:

Rating:

Earnings Calendar

Earnings Calendar  Economic Calendar

Economic Calendar  VAT Calculator

VAT Calculator  Tax Free Childcare Calculator

Tax Free Childcare Calculator Percentage Calculator

Percentage Calculator Compound Interest Calculator

Compound Interest Calculator  Loan Overpayment Calculator

Loan Overpayment Calculator Mortgage Calculator

Mortgage Calculator Credit Card Calculator

Credit Card Calculator

Investing

Investing  Economics

Economics Trading

Trading  Technical Analysis

Technical Analysis  Personal Finance

Personal Finance Calculator

Calculator