Microsoft (MSFT): AI Leadership Supports Long-Term Growth

$396.94

21 Jul 2026, 22:43

Neutral

Join Minipip Academy and access free courses in investing, trading, economics, and more.

Sign Up

Front Page

Moderna emerged as one of the defining biotechnology companies of the pandemic era, transforming messenger RNA technology from a largely experimental platform into a globally recognised medical innovation. Yet the post-pandemic environment presents a fundamentally different challenge as revenues begin to normalise.

Bottom-Up Fundamentals: The Microeconomics of the Company

Moderna currently reflects many of the structural valuation characteristics commonly associated with late-stage developmental biotechnology firms transitioning toward a broader multi-product commercial structure. Unlike mature cash-generative corporations, Moderna’s present financial profile is dominated by substantial research expenditure, pipeline reinvestment, and post-pandemic revenue normalisation, resulting in negative earnings and the temporary breakdown of traditional valuation metrics such as P/E and PEG ratios.

At present, the company trades at approximately $49.48 per share, with a market capitalisation fluctuating between roughly $19.5 billion and $20 billion depending upon intra-day trading activity. Trailing twelve-month earnings remain deeply negative at approximately -$3.19 billion, while diluted EPS sits near -8.15. Forward expectations similarly remain negative, with projected EPS estimates around -4.73, reflecting continued developmental expenditure and anticipated near-term cash outflow across Moderna’s broader mRNA pipeline.

Consequently, conventional valuation tools such as trailing and forward P/E ratios become analytically limited in this context. While the raw trailing calculation approximates -6.19x, these metrics struggle to contextualise developmental expenditure against the probability-adjusted future value of therapeutic success, regulatory approval, and commercial adoption.

Moderna’s negative earnings yield of approximately -16.14% may indicate operational inefficiencies, though considering R&D requirements of the sector, it is more likely to reflect aggressive reinvestment into long-term development.

Top-Down Fundamentals: Macroeconomics of the Sector

Although formally classified within the healthcare sector, industry classification remains essential when analysing how institutional capital rotates between traditionally defensive healthcare exposure and higher-risk biotechnology assets. Moderna behaves less like a conventional defensive healthcare stock, whose relatively stable patient demand may help sustain cash flows during weaker economic cycles, and more like a long-duration biotechnology asset whose valuation is heavily dependent on future clinical successand market sentiment rather than current profitability. Moderna’s own pipeline shows commercial respiratory products alongside Phase 3 flu, pandemic flu, norovirus and oncology programmes, reinforcing the idea that the investment case is now pipeline-led rather than COVID-led.

The interest-rate environment is therefore central. Higher rates increase the discount applied to future cash flows, which pressures companies whose value sits far in the future. This affects Moderna through three channels: valuation compression, financing sensitivity and cash-runway management. The company had $7.5bn in cash and investments at 31 March 2026, down from $8.1bn at year-end 2025, while projected year-end 2026 cash and investments are $4.5bn–$5.0bn, excluding further credit-facility drawdowns. It also secured a five-year $1.5bn Ares loan, drawing $600m upfront with further tranches available through 2027 and 2028, which improves flexibility but introduces greater sensitivity to credit conditions.

Inflation and the economic cycle affect Moderna asymmetrically. Healthcare demand is less directly cyclical than consumer discretionary demand as healthcare services are essential and continuously needed irrespective of whether the economic cycle is booming or crashing. But biotechnology financing is highly cyclical because investors rotate away from speculative, loss-making companies when liquidity tightens.

Moderna’s response has been cost discipline: 2026 R&D is guided at approximately $3.0bn, Selling General & Administrative expenses (SG&A) at approximately $1.0bn, and management has targeted expense reductions while working toward a breakeven point in the books.

Moderna is highly exposed to a wide range of variables such as: vaccine uptake, public-health procurement, foreign-exchange effects, credit spreads, regulatory outcomes, and broader investor risk appetite, meaning price appreciation may remain heavily sentiment- and catalyst-driven rather than purely earnings-driven, although forward EPS projections suggest analysts still expect medium-term financial improvement

Analyst Consensus & Market Expectations

Current analyst recommendations remain heavily concentrated toward neutrality, consisting of Buy: 1, Hold: 13, and Sell: 1. Price targets similarly reflect a broad dispersion of expectations, illustrating how analyst disagreement tends to widen when valuation depends more heavily on future projections than present financial stability. Current estimates range from a bullish target of $69 to a bearish target of $32, with an average target of approximately $44.73, implying a consensus downside of roughly -10.6% from current price levels.

The relatively narrow number of bullish recommendations suggests that many analysts remain unconvinced about near-term earnings recovery or immediate commercial scalability outside COVID-related products. At the same time, the absence of widespread sell ratings indicates that institutional analysts still recognise the long-term strategic potential of Moderna’s mRNA platform.

Price Action & Technical Analysis

From a technical perspective, Moderna currently appears to be transitioning between long-term structural weakness and a tentative medium-term stabilisation phase. The broader chart remains heavily influenced by the post-pandemic unwinding of COVID-driven momentum, although recent price action suggests that bearish pressure has moderated relative to prior periods.

The EMA structure presently shows:

with the shorter-term averages positioned above the longer-term average in a bullish alignment (20 > 50 > 100).

The flattening behaviour of the 20 EMA indicates that short-term momentum is weakening rather than strengthening aggressively, and the market currently appears less like a strong bullish trend and more like a shallow recovery or consolidation phase within a broader long-term downtrend.

This interpretation can be juxtaposed with the Directional Movement Index:

The near-equilibrium between buyers and sellers, combined with a relatively weak ADX reading below 20, suggests the absence of a strong directional trend. In practical terms, this implies that although buyers maintain a slight advantage, conviction remains limited and the market lacks sustained trend strength.

Momentum indicators further support this cautious interpretation.

Although both MACD readings remain in negative territory:

the MACD line is positioned above the signal line suggesting that bearish momentum has been moderating and while the market may still be structurally weak on a broader basis, the short-term downside pressure has eased relative to previous periods.

However, because both values remain below the zero line, the signal does not yet confirm a fully established bullish trend.

Meanwhile, the RSI near 47 reflects broadly neutral sentiment, neither oversold nor overbought, potentially indicating consolidation rather than trend continuation.

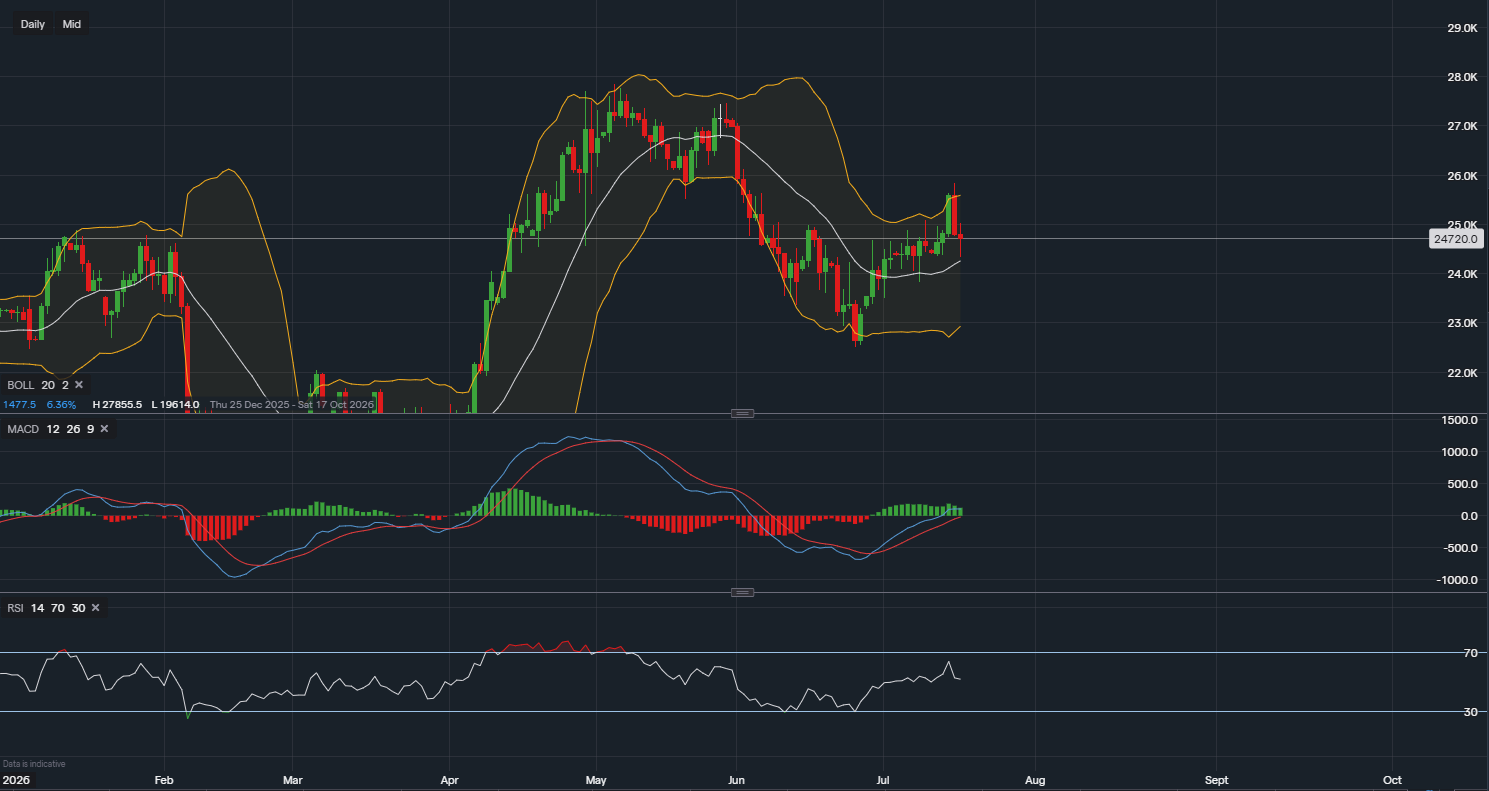

Bollinger Bands also illustrate contracting volatility conditions:

The relatively compressed band structure suggests that Moderna is currently trading within a lower-volatility phase. Such contractions can frequently precede larger directional moves, although the indicators presently do not strongly confirm either a bullish breakout or bearish continuation.

Technically, the 100 EMA currently acts as a support region, while the upper Bollinger Band functions as a near-term resistance zone. Higher confluence across indicators and timeframes could suggest a higher probability of a shift in price action, for example: a medium-term recovery may be forecasted by a breakout beyond resistance, accompanied by a rising ADX and bullish MACD confirmation.

Conversely, rejection near resistance combined with renewed bearish momentum could reinforce the longer-duration downtrend that has dominated Moderna since pandemic-related growth expectations began to unwind.

Summary

Healthcare sector: potentially defensive in slow-growth or risk-off periods.

Biotech subsector: more sensitive to rates, liquidity and clinical catalysts.

Moderna: likely improving if relative momentum continues, but not yet a confirmed structural leader unless it sustains relative strength versus key benchmarks such as the State Street SPDR S&P Biotech ETF, iShares Biotechnology ETF and the S&P 500.

Educational Disclaimer

This content is for educational and informational purposes only and should not be considered financial advice. Always conduct independent research or consult a qualified financial professional before making investment decisions.

Tradable assets:

Min.Deposit:

Max Leverage:

FCA:

Rating:

Earnings Calendar

Earnings Calendar  Economic Calendar

Economic Calendar  VAT Calculator

VAT Calculator  Tax Free Childcare Calculator

Tax Free Childcare Calculator Percentage Calculator

Percentage Calculator Compound Interest Calculator

Compound Interest Calculator  Loan Overpayment Calculator

Loan Overpayment Calculator Mortgage Calculator

Mortgage Calculator Credit Card Calculator

Credit Card Calculator

Investing

Investing  Economics

Economics Trading

Trading  Technical Analysis

Technical Analysis  Personal Finance

Personal Finance Calculator

Calculator