Microsoft (MSFT): AI Leadership Supports Long-Term Growth

$396.94

21 Jul 2026, 22:43

Neutral

Join Minipip Academy and access free courses in investing, trading, economics, and more.

Sign Up

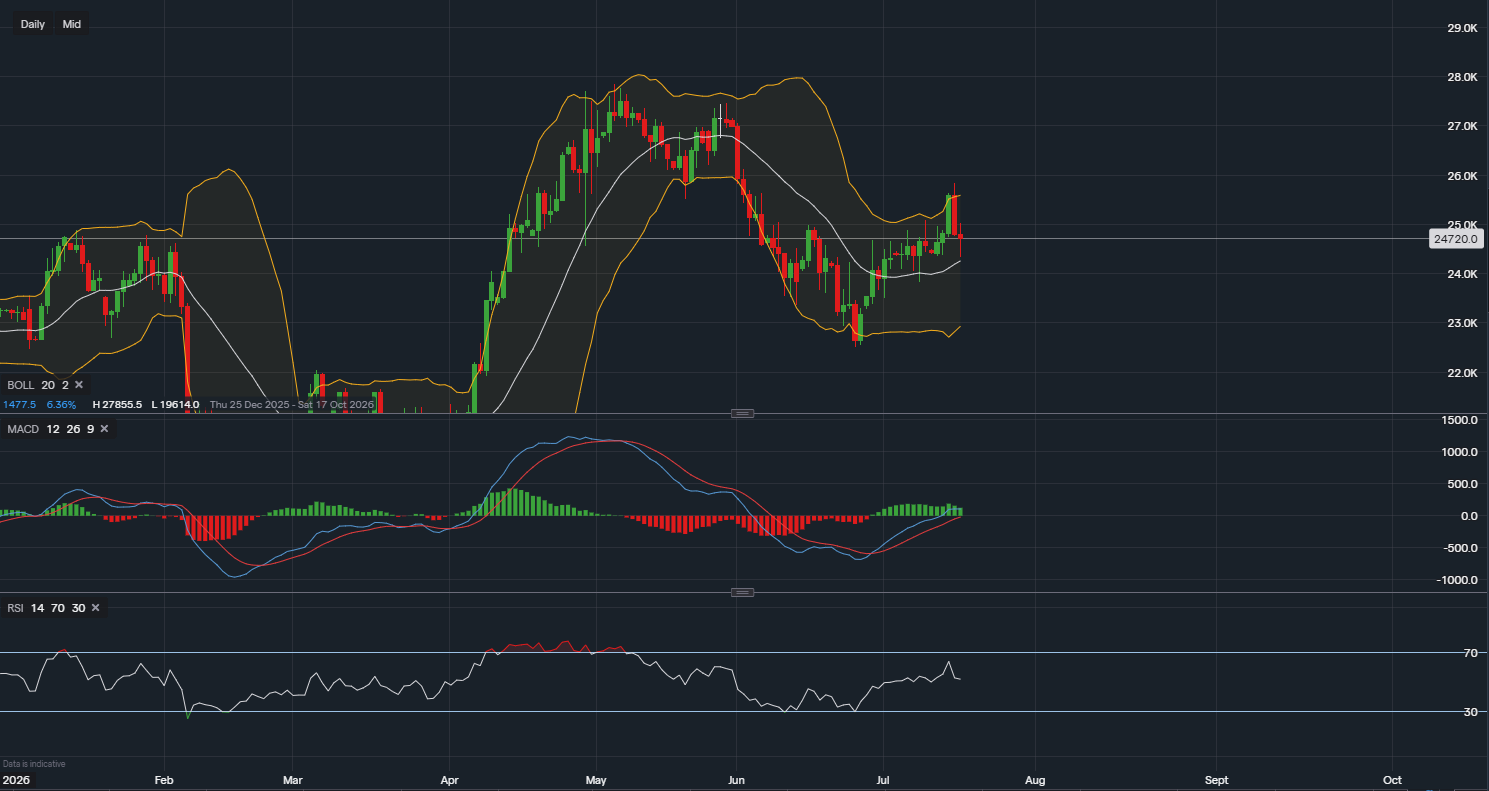

Chart & Data from IG

Netflix shares have come under renewed pressure following the company’s Q4 2025 earnings report, which triggered a negative reaction from investors. The sell-off has pushed the stock lower, with shares trading around $83.69 in pre-market trading, placing Netflix at a key technical support zone as broader market sentiment begins to deteriorate.

This article combines technical analysis and fundamental analysis to assess where Netflix stock could be headed next.

Following the earnings release, Netflix stock has fallen into a critical $81–$85 support range, a zone that previously held during last year’s tariff-driven market sell-off. So far, price action suggests this area is holding, but downside risks remain elevated.

Market sentiment has weakened amid heightened geopolitical uncertainty surrounding Greenland, reducing investor appetite for risk assets. This deterioration in sentiment has weighed heavily on growth stocks, including Netflix.

Adding to the pressure is the ongoing Warner Bros deal, which remains unresolved and could extend for several more months, keeping uncertainty elevated.

From a technical perspective, a decisive break below the $81–$85 support zone could open the door to a deeper pullback. In that scenario, Netflix shares may retrace towards the $65–$70 region.

On the weekly timeframe, this lower range aligns closely with where the 200-day moving average is expected to sit, making it a key area of longer-term technical support — but only if the stock breaks lower first.

One notable development is the Relative Strength Index (RSI) on the weekly chart, which is currently at its most oversold level since 2022. While this could suggest downside momentum is becoming stretched, Netflix shares have historically been able to remain oversold for extended periods before forming a durable bottom.

As a result, short-term caution remains warranted, and the technical bias continues to favour the bears.

For the bearish technical bias to weaken, Netflix would need to reclaim higher levels convincingly. A sustained move above $90 per share would help fade recent concerns, improve sentiment, and potentially signal a rebuilding of bullish momentum.

From a fundamental standpoint, Netflix’s Q4 2025 financial results present a mixed picture, combining strong revenue growth with margin pressure and slowing earnings momentum.

Netflix reported Q4 2025 revenue of $12.05 billion, up from $11.51 billion in Q3 2025 and $10.25 billion in Q4 2024, highlighting continued top-line growth.

For the full year 2025, total revenue reached approximately $45.18 billion, reinforcing the strength of Netflix’s subscription model and its global content strategy.

Despite higher revenues, operating costs increased at a faster pace:

Cost of revenues: $6.52 billion

Sales and marketing: $1.11 billion

Technology and development: $890 million

General and administrative: $568 million

This led to operating income of $2.96 billion in Q4 2025, down from $3.25 billion in Q3 2025, signalling margin compression.

Netflix continues to invest heavily in content creation, platform technology, and marketing, which supports long-term competitiveness but weighs on near-term profitability.

Netflix posted net income of $2.42 billion in Q4 2025, compared with $2.55 billion in the previous quarter.

Diluted EPS declined to $0.56, down from $0.59 in Q3

Full-year 2025 diluted EPS came in at $2.53

The slowdown in earnings growth relative to revenue expansion likely contributed to the negative investor response following the earnings release.

Fundamentally, Netflix remains a profitable and growing business, but the balance between growth investment and operational efficiency is becoming a key concern for investors.

Fundamental positives:

Strong and consistent revenue growth

Global scale and pricing power

Healthy absolute profitability

Fundamental risks:

Rising operating costs

Margin compression

Slowing EPS growth

In the near term, fundamentals do not yet provide a clear bullish catalyst, aligning with the current bearish technical setup.

When combining both technical and fundamental analysis, the outlook for Netflix remains cautiously bearish in the short term. Technical indicators point to downside risk if key support fails, while fundamentals suggest investors may remain cautious until margin trends stabilise.

A sustained recovery above $90 per share, or evidence of improving cost control in upcoming quarters, would be needed to shift the overall outlook more decisively bullish.

Until then, Netflix stock is likely to remain volatile, with both traders and long-term investors watching key support levels closely.

(Disclaimer: Not to be interpreted, taken, used as financial advice)

Tradable assets:

Min.Deposit:

Max Leverage:

FCA:

Rating:

Earnings Calendar

Earnings Calendar  Economic Calendar

Economic Calendar  VAT Calculator

VAT Calculator  Tax Free Childcare Calculator

Tax Free Childcare Calculator Percentage Calculator

Percentage Calculator Compound Interest Calculator

Compound Interest Calculator  Loan Overpayment Calculator

Loan Overpayment Calculator Mortgage Calculator

Mortgage Calculator Credit Card Calculator

Credit Card Calculator

Investing

Investing  Economics

Economics Trading

Trading  Technical Analysis

Technical Analysis  Personal Finance

Personal Finance Calculator

Calculator